Improving Performance

# packages neededlibrary(tidyverse) # for bench packagelibrary(parallel)library(MonteCarlo)

# packages neededlibrary(tidyverse) # for bench packagelibrary(parallel)library(MonteCarlo)We should forget about small efficiencies, say about 97% of the time: premature optimisation is the root of all evil. Yet we should not pass up our opportunities in that critical 3%. A good programmer will not be lulled into complacency by such reasoning, he will be wise to look carefully at the critical code; but only after that code has been identified. — Donald Knuth

Improving Performance — Golden Rule

Before we continue, we introduce a rule we have already followed implicitly: the golden rule of R programming:

Access the underlying C/FORTRAN routines as quickly as possible; the fewer functions calls required to achieve this, the better.

(Lovelace and Gillespie, 2016)

The techniques discussed next follow this paradigm. If this is not enough, we still may rewrite (some of) the code in C++ using the Rcpp package (discussed in the next chapter).

2. Do as Little as Possible

If you cannot find existing solutions, start by reducing your code to the bare essentials.

Exercise: coercion of inputs / robustness checks

X <- matrix(1:1000, ncol = 10)Y <- as.data.frame(X)Which approach is faster and why?

apply(X, 1, sum)apply(Y, 1, sum)2. Do as Little as Possible

A function is faster if it has less to do — obvious but often neglected!

Use functions tailored to specific input and output types / specific problems!

Exercise: coercion of inputs / robustness checks — ctd.

Which approach is faster and why?

rowSums(X)apply(X, 1, sum)2. Do as Little as Possible

Exercise: Linear Regression — computation of

Which approach is faster and why? Name disadvantages of the fastest one.

set.seed(1)X <- matrix(rnorm(100), ncol = 1)Y <- X + rnorm(100)a <- function() { coefficients(summary(lm(Y ~ X - 1)))[1, 2] }b <- function() { fit <- lm.fit(X, Y) c( sqrt(1/(length(X)-1) * sum(fit$residuals^2) * solve(t(X) %*% X)) )}2. Do as Little as Possible

Be as explicit as possible.

Example: method dispatch takes time

x <- runif(1e2)bench::mark( mean(x), mean.default(x))## # A tibble: 2 x 6## expression min median `itr/sec` mem_alloc `gc/sec`## <bch:expr> <bch:tm> <bch:tm> <dbl> <bch:byt> <dbl>## 1 mean(x) 2.64µs 3.07µs 297320. 22.7KB 0 ## 2 mean.default(x) 1.13µs 1.35µs 659992. 0B 66.02. Do as Little as Possible

Benchmark against alternatives that rely on primitive functions.

Example: primitives are faster

bench::mark( mean.default(x), sum(x)/length(x))## # A tibble: 2 x 6## expression min median `itr/sec` mem_alloc `gc/sec`## <bch:expr> <bch:tm> <bch:tm> <dbl> <bch:byt> <dbl>## 1 mean.default(x) 1.15µs 1.38µs 658724. 0B 0## 2 sum(x)/length(x) 432ns 526ns 1637111. 0B 02. Do as Little as Possible — Exercises

- Can you come up with an even faster implementation of

b()in the linear regression example?

What’s the difference between

rowSums()and.rowSums()?rowSums2()is an alternative implementation ofrowSums(). Is it faster for the inputdf? Why?rowSums2 <- function(df) {out <- df[[1L]]if (ncol(df) == 1) return(out)for (i in 2:ncol(df)) {out <- out + df[[i]]}out}df <- as.data.frame(replicate(1e3, sample(100, 1e4, replace = TRUE)))

2. Do as Little as Possible — Case Study

Imagine you want to compute the bootstrap distribution of a sample correlation coefficient using cor_df() and the data in the example below.

Given that you want to run this many times, how can you make this code faster?

n <- 1e6df <- data.frame(a = rnorm(n), b = rnorm(n))cor_df <- function(df, n) { i <- sample(seq(n), n, replace = TRUE) cor(df[i, , drop = FALSE])[2, 1]}3. Vectorise your code

Why is vectorisation efficient? — ctd.

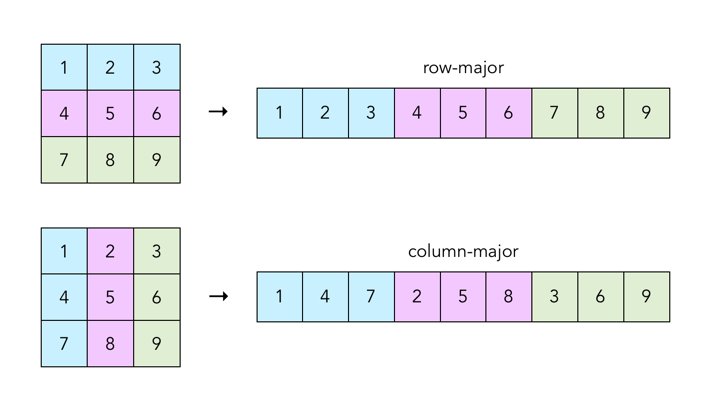

Many languages (including R) work on arrays that are stored in the memory in column-major order.

Disregarding these patterns by writing code which operates on vectors thus means 'fighting the language'.

3. Vectorise your code

What does it mean to write 'vectorised' code in R?

Remember that there are no 'real' scalars in R. Everything that looks like a scalar is actually a vector.

# otherwise this shouldn't work:1[1]## [1] 1Thus 'scalar' operations work on vector elements which is (often) needlessly cumbersome.

3. Vectorise your code

What does it mean to write 'vectorised' code in R?

By 'vectorised' we mean that the function works on vectors, i.e., performs vector arithmetic and calls functions which work on vectors.

Example: scalar vs. vectorised computation of euclidean norm

L2_scalar <- function(x) { out <- numeric(1) for(i in 1:length(x)) { out <- x[i] * x[i] + out } return(sqrt(out))}L2_vec <- function(x) { return( sqrt( sum(x * x) ) )}3. Vectorise your code

What does it mean to write 'vectorised' code in R?

By 'vectorised' we mean that the function works on vectors, i.e., performs vector arithmetic and calls functions which work on vectors.

Example: scalar vs. vectorised computation of euclidean norm

bench::mark( L2_scalar(1:1e4), L2_vec(1:1e4))## # A tibble: 2 x 6## expression min median `itr/sec` mem_alloc `gc/sec`## <bch:expr> <bch:tm> <bch:tm> <dbl> <bch:byt> <dbl>## 1 L2_scalar(1:10000) 713.1µs 775.8µs 1236. 4.11MB 0 ## 2 L2_vec(1:10000) 40.3µs 73.1µs 12708. 78.22KB 16.93. Vectorise your code

Example: avoid growing objects

3. Vectorise your code

Example: good and bad for() loops

# Bad: c()/cbind()/rbind()rw_bad <- function(N) { set.seed(1) out <- rnorm(1) for(i in 2:N) { out <- c(out, out[i-1] + rnorm(1)) } return(out)}

3. Vectorise your code

Example: good and bad for() loops

# Good: proper initialisation/iterationrw_good <- function(N) { set.seed(1) out <- vector("double", N) out[1] <- rnorm(1) for(i in 2:N) { out[i] <- rnorm(1) + out[i-1] } return(out)}

3. Vectorise your code

Example: good and bad for() loops

bench::mark(rw_good(1e4), rw_bad(1e4))## # A tibble: 2 x 6## expression min median `itr/sec` mem_alloc `gc/sec`## <bch:expr> <bch:tm> <bch:tm> <dbl> <bch:byt> <dbl>## 1 rw_good(10000) 15.2ms 22.6ms 39.3 24.8MB 21.6## 2 rw_bad(10000) 346ms 351.5ms 2.85 406.3MB 27.03. Vectorise your code

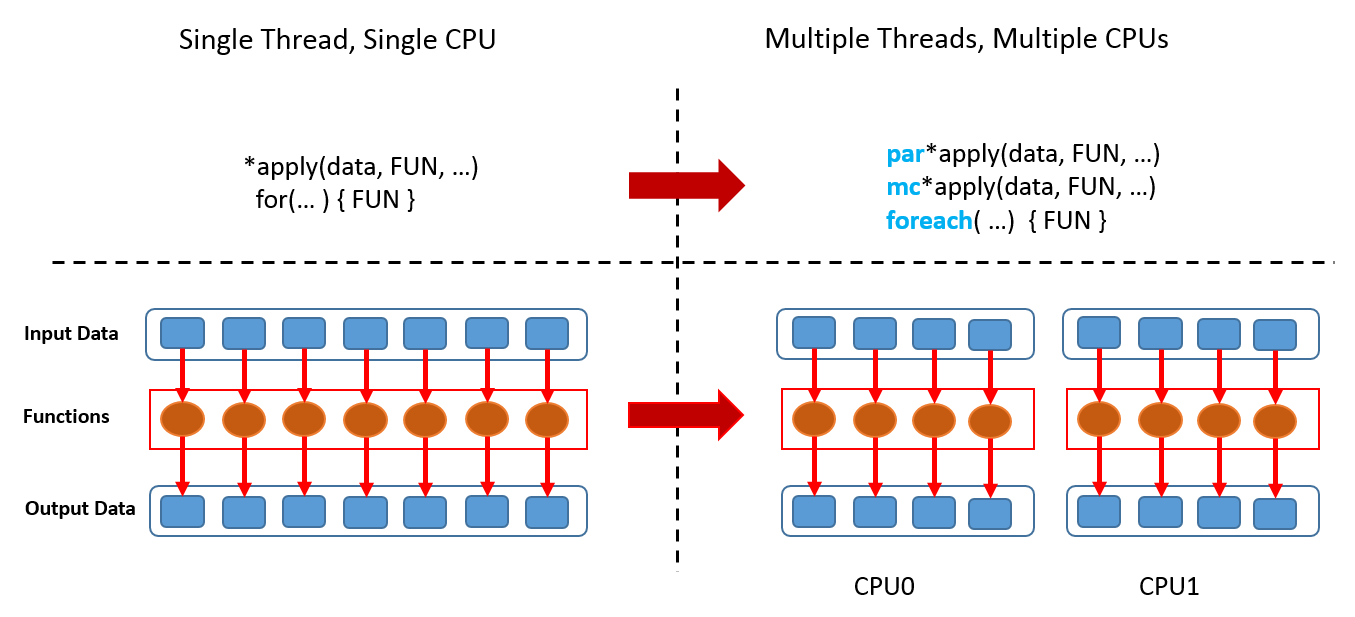

Are for() loops slower than the *apply() functions?

Example: for() vs. apply()

X <- matrix(rnorm(1e4), ncol = 1e4)colmax <- function(x) { out <- numeric(ncol(x)) for(j in 1:ncol(x)) { out[j] <- max(x[,j]) } return(out)}3. Vectorise your code

Are for() loops slower than the *apply() functions?

Example: for() vs. apply() — ctd.

bench::mark( colmax(X), apply(X, 2, max))## # A tibble: 2 x 6## expression min median `itr/sec` mem_alloc `gc/sec`## <bch:expr> <bch:tm> <bch:tm> <dbl> <bch:byt> <dbl>## 1 colmax(X) 5.75ms 6.37ms 156. 4.34MB 55.0## 2 apply(X, 2, max) 9.05ms 10.27ms 96.6 312.73KB 55.24. Parallelisation — the parallel package

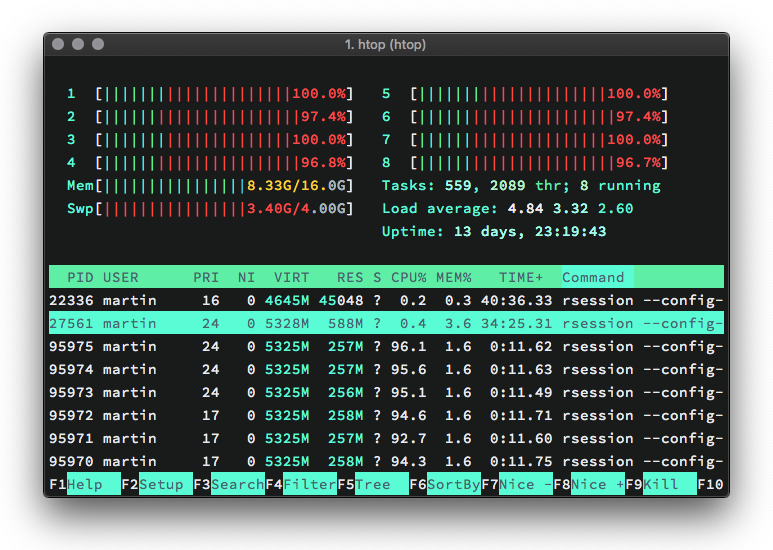

The parallel package (comes with base R) is a good starting point for parallel computing.

# detect numer of cores (including logical cores)library(parallel)detectCores()## [1] 8The notebook used to run this script has a 2,3 GHz Intel Core i5 processor with 4 physical CPUs and supports hyper-threading, i.e., each CPU has 2 logical cores.

# detect numer of physical coresdetectCores(logical = F)## [1] 4Note that the behavior of detectCores() is platform specific and not always reliable, see ?detectCores().

4. Parallelisation - parallel::mclapply()

Example: send them cores to sleep (on MacOS)

r <- mclapply(1:8, function(i) Sys.sleep(20), mc.cores = 8)

4. Parallelisation - parallel::mclapply()

Example: send them cores to sleep (Windows)

An alternative on Windows is to use parallel::parLapply(). The setup is somewhat more complex.

# set number of cores to be usedcores <- detectCores(logical = TRUE) - 1# initialize clustercl <- makeCluster(cores)# run lapply in parallelparLapply(cl, 1:8, function(i) Sys.sleep(20))# stop clusterstopCluster(cl)

4. Parallelisation

Example: parallelised bootstrapping

Remember the function cor_df() from the case study in 2. Do as Little as Possible. A faster approach, cor_df2(), is given below.

n <- 1e4df <- data.frame(a = rnorm(n), b = rnorm(n))cor_df2 <- function(x, n) { i <- sample.int(n, n, replace = T) cor(df$a[i], df$b[i])}4. Parallelisation

Example: parallelised bootstrapping — ctd.

Calling cor_df2() a large number of times is time consuming.

# serial computations_ser <- system.time( r_ser <- lapply(1:1e5, function(x) cor_df2(df, n)))s_ser## ## user system elapsed ## 41.258 7.497 48.8354. Parallelisation

Example: parallelised bootstrapping — ctd.

Luckily, it is straightforward to bootstrap in parallel using mclapply().

# parallel computations_par <- system.time( r_par <- mclapply(1:1e5, function(x) cor_df2(df, n), mc.cores = 8))s_par## ## user system elapsed ## 38.343 7.995 16.343Note that using 8 cores in my case is (only) ~5 times faster than the serial approach due to overhead.

4. Parallelisation

Example: too much overhead

Parallelisation may be inefficient:

system.time(mclapply(1:1e5, sqrt, mc.cores = 8))## ## ## user system elapsed ## ## 0.107 0.110 0.062 ##system.time(lapply(1:1e5, sqrt))## ## ## user system elapsed ## ## 0.034 0.001 0.035 ##This is because the cost of the individual computations is low, and additional work is needed to send the computation to the different cores and to collect the results: The overhead exceeds the time savings.

4. The MonteCarlo Package

Example: Unit Root test — ctd.

We use the MonteCarlo package to simulate the limit distribution of .

library(MonteCarlo)sim <- function(rho, Time) { Y <- matrix(NA_real_, ncol = 1, nrow = Time); Y[1,1] <- rnorm(1) for(t in 2:Time) { Y[t, 1] <- rho * Y[t-1, 1] + rnorm(1) } y <- Y[-1, , drop = FALSE] ylag <- Y[-Time, , drop = FALSE] fit <- lm.fit(ylag, y) rho <- fit$coefficients res <- fit$residuals sigma <- sqrt(1/(Time-2) * t(res) %*% res * 1/ (t(ylag) %*% ylag)) return( list("t" = (rho[[1]] - 1)/sigma) )}4. The MonteCarlo Package

Example: Unit Root test — ctd.

# setup list of parametersparams <- list("rho" = 1, "Time" = 1000)# run parallelised MC simulation over parameter gridr <- MonteCarlo( sim, nrep = 50000, param_list = params, ncpus = parallel::detectCores())We transform the simulated test statistics to a vector.

t_sim <- apply(r$result$t, 3, c)4. The MonteCarlo Package

Example: Unit Root test — ctd.

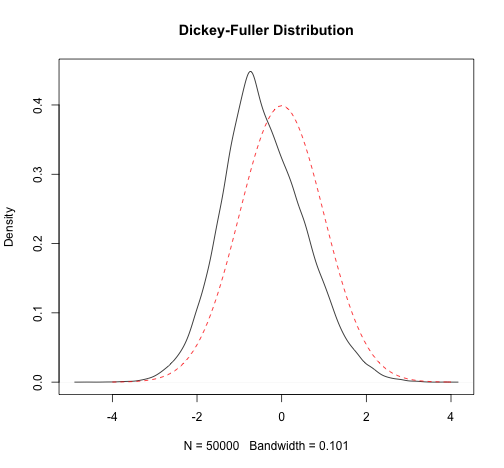

Estimates of the finite sample quantiles are close to the quantiles of the corresponding asymptotic Dickey-Fuller distribution

quantile(t_sim, c(0.05, 0.1, 0.5, 0.9, 0.95))## 5% 10% 50% 90% 95% ## -1.9472738 -1.6124977 -0.5044926 0.8846489 1.2702348fUnitRoots::qunitroot(c(0.05, 0.1, 0.5, 0.9, 0.95), trend = "nc")## [1] -1.9408468 -1.6167526 -0.4999276 0.8877673 1.2836012We compare with the Gaussian distribution.

plot(density(t_sim), main = "Dickey-Fuller Distribution")curve(dnorm(x), from = -4, to = 4, add = T, lty = 2, col = "red")4. The MonteCarlo Package

Example: Unit Root test — ctd.

4. The MonteCarlo Package

It is a great benefit to work with the package if you want to run the simulation for several parameter combinations.

Example: Power of DF-Test

We write a simple wrapper for sim() which returns a logical value for rejection at 5% using the asymptotic critical value.

# asymptotic 5% critical value of the corresponding DF-distributioncrit <- fUnitRoots::qunitroot(0.05, trend = "nc")# rejection?sim_pow <- function(rho, Time) { return( list("t" = sim(rho, Time)[[1]] < crit) )}4. The MonteCarlo Package

Example: Power of DF-Test — ctd.

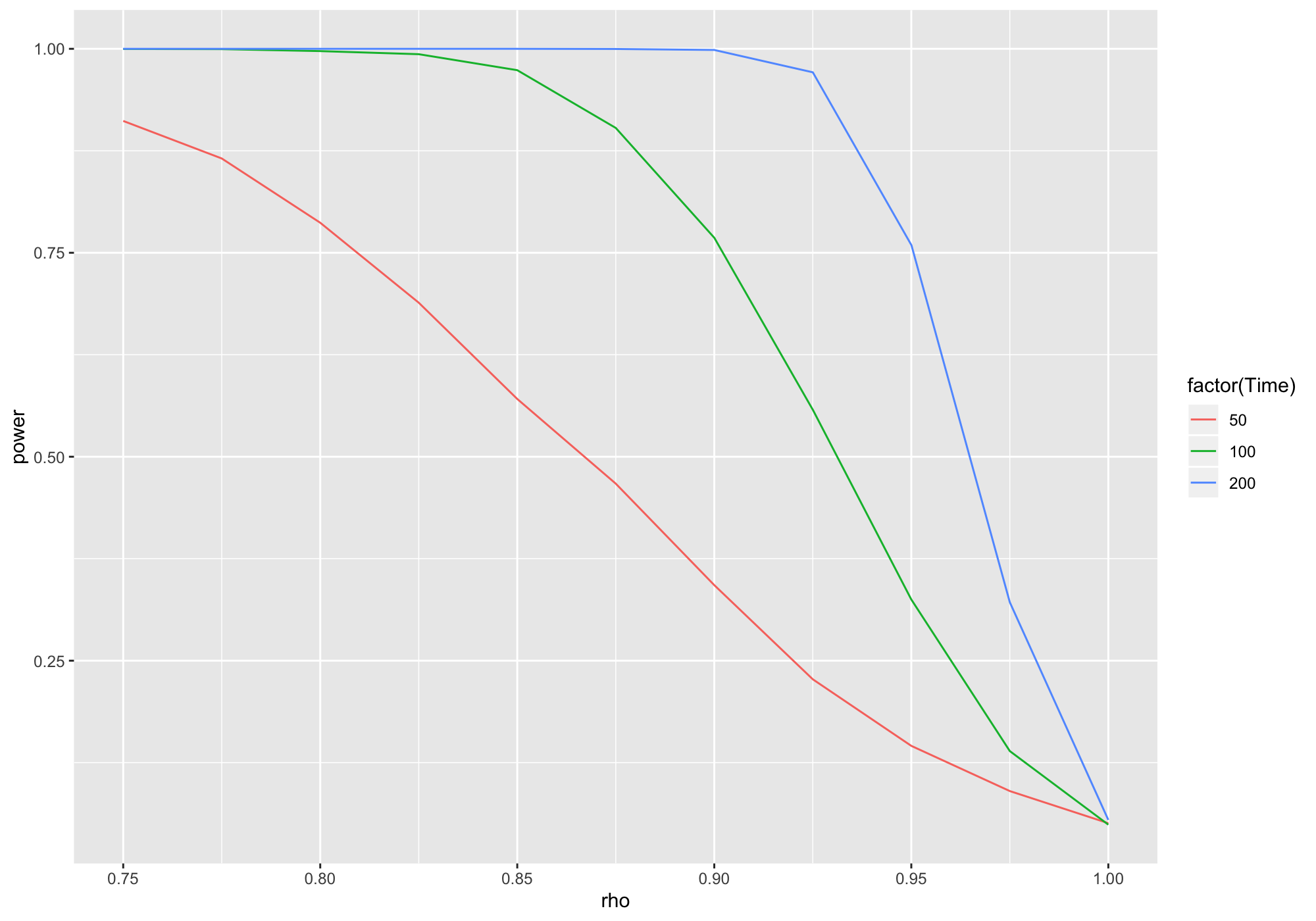

We consider all combination for a sequence of alternatives and three different sample sizes.

# setup list of parameters (yielding 33 parameter constellations)params <- list("rho" = seq(0.75, 1, 0.025), "Time" = c(50, 100, 200))# run parallelised MC simulation over parameter gridr <- MonteCarlo( sim_pow, nrep = 5000, param_list = params, ncpus = parallel::detectCores())4. The MonteCarlo Package

Example: Power of DF-Test — ctd.

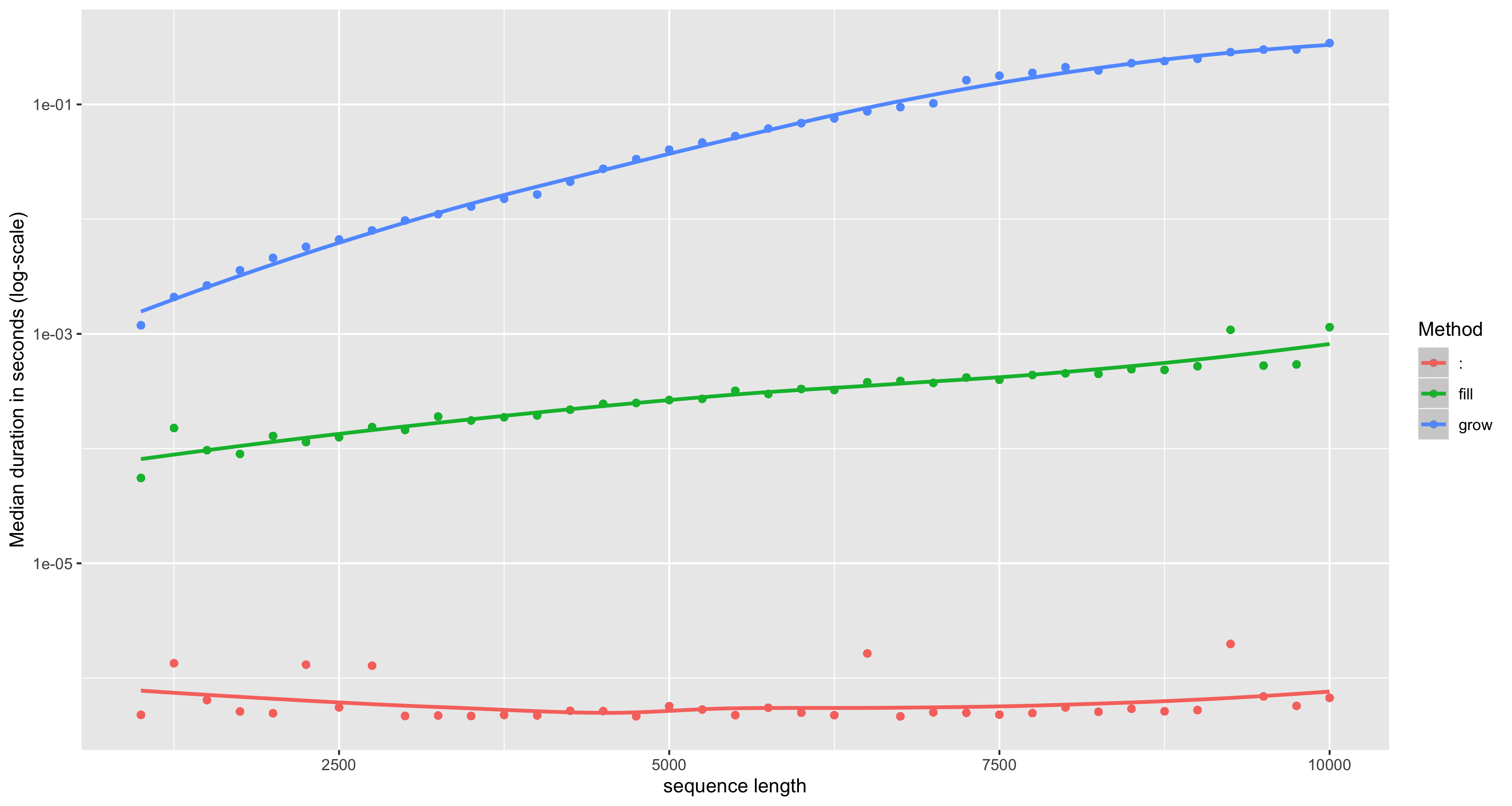

Content of a MonteCarlo object is easily transformed and visualised using tidyverse functions.

library(dplyr)library(ggplot2)tbl <- r %>% MakeFrame() %>% tbl_df() %>% group_by(rho, Time) %>% summarise(power = mean(t))ggplot(tbl) + geom_line(aes(x = rho, y = power, col = factor(Time)))4. The MonteCarlo Package

Example: Power of DF-Test — ctd.

4. The MonteCarlo Package

Example: Power of DF-Test — ctd.

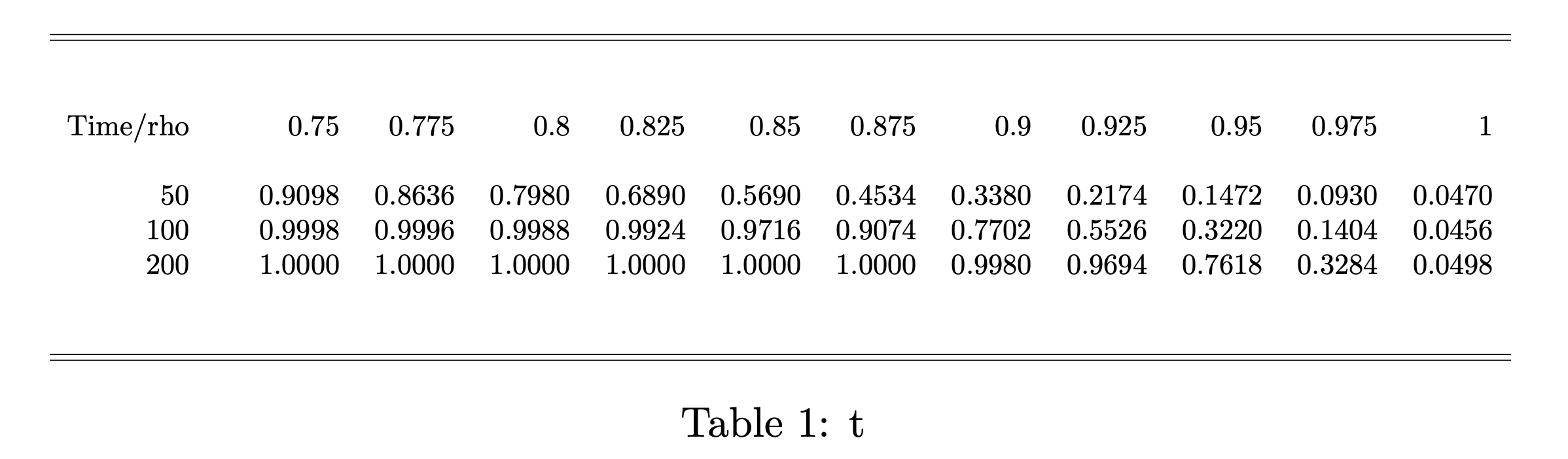

Conversion of the results into a table is particularly useful.

# generate LaTeX table from simulation resultsMakeTable(r, rows = "Time", "rho")